Construction Revenue Recognition: The Ultimate Guide to ASC 606 & Profitability

Are manual spreadsheets and the looming threat of ASC 606 non-compliance eroding your confidence? For many construction firms, inaccurate financial reporting isn't just a headache-it's a direct threat to profitability, leading to poor decisions and shrinking margins. The root of this challenge often lies in a complex, yet critical, process: construction revenue recognition. Getting it wrong means flying blind, but mastering it unlocks a powerful new level of financial control and strategic visibility.

This ultimate guide is your roadmap. We will demystify the ASC 606 standards and provide a clear framework for choosing the right method for your projects. You will learn how to replace error-prone manual calculations with a robust, automated system that provides a real-time 'single source of truth' for project costs and progress. Prepare to achieve full compliance, gain unparalleled insight into project profitability, and make more confident financial decisions that drive your business forward.

Why Revenue Recognition is a High-Stakes Game in Construction

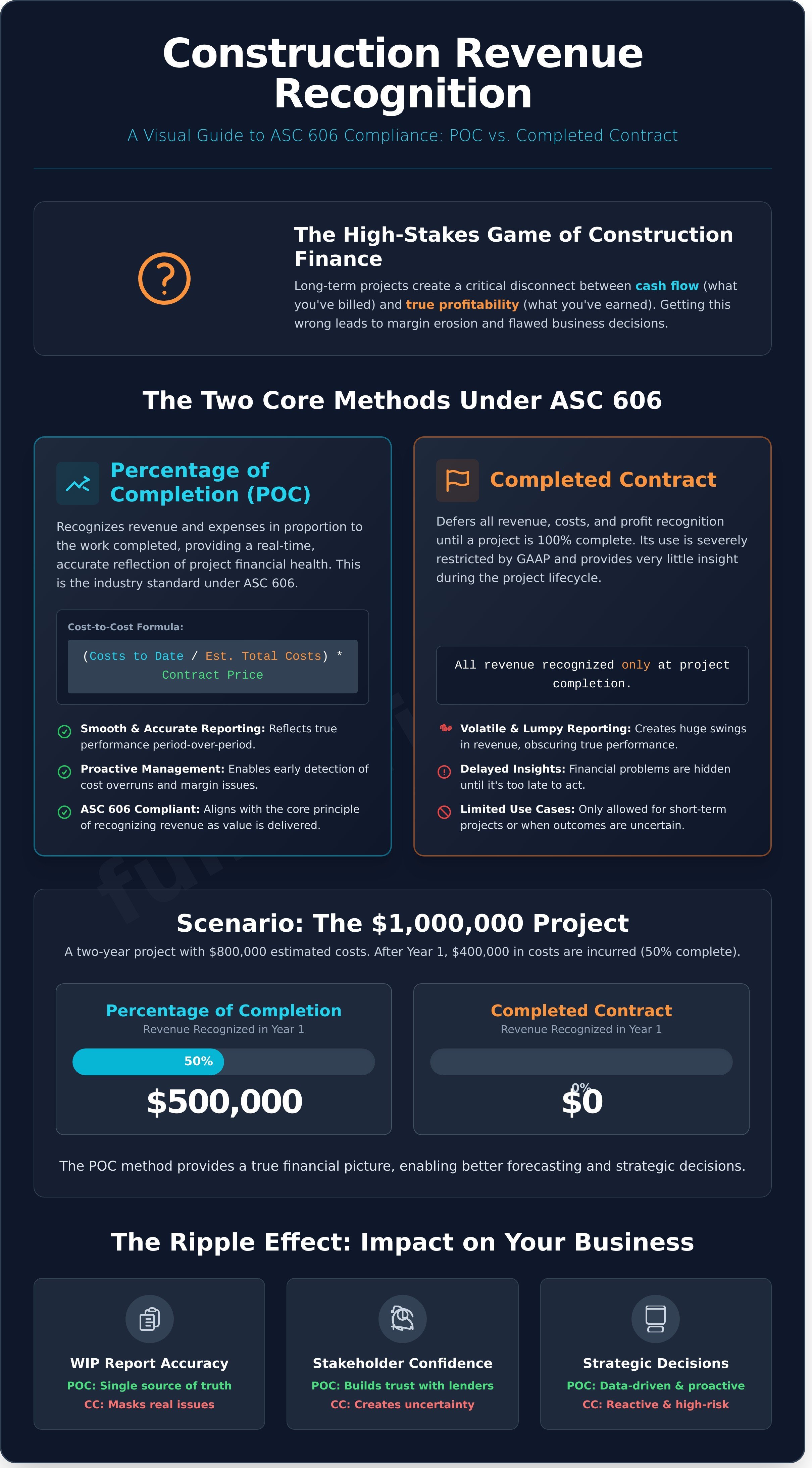

Unlike a simple retail transaction, construction projects unfold over months or years, creating a critical disconnect between cash flow (what you’ve billed) and true profitability (what you’ve earned). Misinterpreting one for the other is a direct path to margin erosion and flawed business decisions. Getting construction revenue recognition right isn’t just an accounting exercise; it’s fundamental to financial survival and growth. Accurate reporting is the bedrock of your ability to secure bonding, access financing, and maintain stakeholder trust.

The Problem with Long-Term, Complex Projects

Selling a finished product is straightforward-revenue is recognized at the point of sale. Building a commercial facility, however, is a dynamic process. Think of it this way: you don't recognize the full value of a house the day you pour the foundation. Over the project lifecycle, you face fluctuating material costs, unexpected change orders, and shifting timelines. Each variable complicates the calculation of earned revenue, making it difficult to get a real-time, accurate picture of financial performance.

ASC 606: The Compliance Mandate You Can't Ignore

The Financial Accounting Standards Board (FASB) provides a robust framework for this complexity through Topic 606 (ASC 606). This standard codifies the core Revenue Recognition Principles, mandating that companies recognize revenue as control of goods or services is transferred to the customer. For construction, this means recognizing revenue progressively as the project is built. Ignoring this mandate isn't an option; non-compliance can trigger severe penalties and costly financial restatements.

Impact on Your Work-in-Progress (WIP) Report

Your WIP report is the ultimate scorecard for project financial health-your real-time single source of truth. The methods you use for revenue recognition directly determine the accuracy of your over/under billings and calculated profit. A WIP report built on flawed data can mask deep-seated issues or create false alarms, leading to poor resource allocation. An accurate, data-driven WIP, however, empowers you to proactively manage costs, protect your margins, and make powerful, forward-looking decisions.

The Core Methods: Percentage of Completion vs. Completed Contract

In construction accounting, the method you use to recognize revenue isn't just a preference-it's a critical decision governed by Generally Accepted Accounting Principles (GAAP), specifically ASC 606. Understanding the two primary approaches, Percentage of Completion (POC) and Completed Contract, is the first step toward achieving financial clarity and compliance. The right choice provides powerful visibility into job profitability and overall business health.

The Percentage of Completion (POC) Method Explained

The Percentage of Completion (POC) method recognizes revenue and expenses in proportion to the progress made on a long-term contract. This approach provides a real-time, accurate reflection of a project's financial performance. The most common way to measure progress is the "cost-to-cost" approach, calculated with a simple formula:

Revenue = (Total Costs to Date / Total Estimated Project Costs) * Total Contract Price

By matching revenue with the costs incurred to generate it, POC delivers a smooth and predictable financial picture, eliminating surprises and empowering proactive management.

The Completed Contract Method Explained

In contrast, the Completed Contract method is far more straightforward but much less insightful. Under this approach, all revenue, costs, and resulting profit are deferred until the project is 100% complete. GAAP severely restricts its use, typically only allowing it for short-term projects (less than one year) or in rare cases where the project's outcome cannot be reliably estimated. Its primary drawback is creating volatile, lumpy financial statements that obscure a company's true performance until a project concludes.

Why POC is the Industry Standard

The POC method is the dominant model for a crucial reason: it aligns directly with the core principle of ASC 606, which mandates that revenue be recognized as performance obligations are satisfied (i.e., as value is delivered to the customer). This makes proper implementation of POC essential for compliant construction revenue recognition. However, navigating contract modifications and variable considerations can be complex, and firms must be diligent to avoid Common ASC 606 Pitfalls that can lead to costly restatements.

Practical Scenario: Applying Both Methods

Imagine a two-year, $1,000,000 project with a total estimated cost of $800,000. At the end of the first year, you have incurred $400,000 in costs.

- Using Percentage of Completion: Your progress is 50% ($400,000 incurred costs / $800,000 total estimated costs). You would recognize $500,000 in revenue for Year 1.

- Using Completed Contract: Despite completing half the physical work, you would recognize $0 in revenue for Year 1. All $1,000,000 would be recognized in Year 2 upon completion.

This stark difference demonstrates how POC provides stakeholders with a true financial picture, enabling better forecasting, bonding capacity, and strategic decision-making.

Mastering the ASC 606 Five-Step Model for Contractors

For construction firms, ASC 606 isn't just a guideline-it's the mandatory framework for financial reporting. This five-step model provides a robust and standardized approach to construction revenue recognition, transforming complex project accounting into a clear, manageable process. Mastering this model is essential for compliance, accurate financial visibility, and protecting your margins on every job.

Let's walk through the model with a real-world example: a $10 million contract to build a small commercial facility.

Steps 1 & 2: Identify the Contract and Performance Obligations

First, confirm you have a contract with enforceable rights and obligations. Next, you must identify each distinct "performance obligation"-the specific promises made to the customer. These are the individual deliverables that provide value. Instead of viewing the project as one massive job, you break it down.

- Example: In the $10M facility project, the distinct performance obligations might be:

- Site preparation and foundation work.

- Structural steel erection and building envelope.

- MEP (Mechanical, Electrical, Plumbing) systems installation.

- Interior finishing and final handover.

Step 3: Determine the Transaction Price

The transaction price is the total compensation you expect to receive. This isn’t just the contract value; it must account for variable considerations. This is a critical step where accurate forecasting prevents future margin erosion. You must estimate and include potential:

- Incentives: Bonuses for early completion.

- Penalties: Fees for schedule delays.

- Change Orders: Anticipated modifications to the scope.

Example: The $10M base contract includes a $200,000 bonus for finishing one month early, which you deem highly probable. The transaction price is therefore estimated at $10.2M.

Steps 4 & 5: Allocate Price and Recognize Revenue

In Step 4, you allocate the total transaction price ($10.2M) across each performance obligation based on its standalone value. In Step 5, you recognize that allocated revenue as each obligation is satisfied. For nearly all construction projects, revenue is recognized over time, typically using a Percentage-of-Completion (POC) method like cost-to-cost.

Example: If the foundation work (Obligation 1) represents 15% of the total project value, you will allocate $1.53M ($10.2M x 15%) to it. As you incur costs to complete the foundation, you recognize a proportional amount of that $1.53M, providing a real-time picture of your financial performance long before the project is complete.

Common Pitfalls in Construction RevRec (And How to Avoid Them)

Mastering the principles of ASC 606 is one thing; executing them flawlessly on active, complex projects is another. Even with the best intentions, common operational gaps can lead to inaccurate financial reporting, compliance risks, and significant margin erosion. Successful firms proactively identify and eliminate these challenges before they impact the bottom line.

Effective construction revenue recognition is not just an accounting exercise-it's a critical component of financial health and project profitability. Here are the most common pitfalls that can derail your efforts and how to build a more resilient process.

Pitfall 1: Inaccurate Job Costing and Estimates

Your revenue recognition is only as accurate as your cost data. When project managers rely on outdated spreadsheets or siloed information, the costs-incurred-to-date are often a guess. This directly corrupts any Percentage of Completion (POC) calculation, leading to misstated financials and poor strategic decisions based on flawed performance metrics.

The Solution: Implement a robust, real-time job costing system. By connecting field data directly to your financial core, you gain immediate visibility into actual costs, enabling you to recognize revenue with confidence and precision.

Pitfall 2: Mismanaging Change Orders and Claims

Unapproved or untracked change orders are a primary source of financial distortion. Under ASC 606, revenue from contract modifications cannot be recognized until they are approved and enforceable. Letting change orders linger in an unapproved state means your recognized revenue doesn't reflect the true scope of work, creating a dangerous gap between reported progress and contractual reality.

The Solution: Digitize and automate your change order workflow. A system that tracks modifications from submission to approval and billing ensures that revenue is recognized in the correct period, maintaining compliance and providing stakeholders with an accurate view of project health.

Pitfall 3: Relying on Disconnected Spreadsheets

Manual data entry, broken formulas, and version control chaos-these are the hallmarks of a spreadsheet-driven process. Spreadsheets create information silos between finance and operations, forcing teams to waste valuable time on manual reconciliation instead of analysis. This manual process is not just inefficient; it's a direct threat to the accuracy of your construction revenue recognition and overall financial integrity.

The Solution: Move to a unified platform that serves as a 'single source of truth'. An integrated cloud ERP system eliminates data silos, automates calculations, and connects every aspect of a project-from the initial bid to the final payment. Learn more about how a solution built on NetSuite provides the visibility and control needed to eliminate these risks and drive profitability.

Automating Revenue Recognition with NetSuite + FullClarity

The manual spreadsheets, data silos, and delayed reports that plague traditional accounting are not inevitable. They are symptoms of a disconnected system-a system that directly contributes to margin erosion. The definitive solution lies in unifying your operations on a single, intelligent platform designed for the complexities of the construction industry. This is where the power of NetSuite + FullClarity transforms your financial processes from a reactive burden into a proactive, strategic advantage.

The Power of a 'Single Source of Truth' ERP

True financial control begins when accounting, job costing, and project management operate from the same real-time data. By leveraging NetSuite as the world's #1 Cloud ERP, you create a robust 'single source of truth.' This seamless integration eliminates duplicate data entry and provides stakeholders-from the field to the back office-with immediate, accurate visibility into project health, ensuring every decision is based on current reality, not outdated reports.

How FullClarity Automates Complex Calculations

FullClarity, built natively on NetSuite, is engineered to master the specific challenges of construction revenue recognition. Our solution eradicates manual calculations and the risk of human error by delivering powerful, automated financial tools. Experience the benefits of a system that provides:

- Automated POC Calculations: The system intelligently calculates Percentage of Completion based on live job cost data, ensuring your revenue is always recognized accurately and in compliance with ASC 606.

- One-Click WIP Reporting: Generate comprehensive and precise Work in Progress reports instantly, giving you a real-time snapshot of your company's financial position without spending days compiling spreadsheets.

- Seamless Document Management: Effortlessly manage critical financial instruments like retainage and certified payroll documents directly within the system, linking them to specific projects for complete auditability.

From Reactive Reporting to Proactive Project Control

Stop managing your projects by looking in the rearview mirror. Monthly spreadsheet reports only tell you where you’ve been, often after it's too late to prevent margin fade. With NetSuite + FullClarity, you gain live dashboards and real-time analytics that empower you to identify potential overruns and protect profitability proactively. Make informed, data-driven decisions that keep your projects on track and on budget. See how Construction for NetSuite provides total financial control.

From Complexity to Clarity: Master Your Construction Revenue Recognition

Ultimately, mastering ASC 606 is about more than just compliance-it’s about gaining strategic control over your profitability. Relying on manual processes and disconnected spreadsheets for something as critical as construction revenue recognition introduces unacceptable risk, from inaccurate reporting to margin erosion. The key takeaway is clear: a unified, automated approach is the only way to ensure accuracy, efficiency, and true financial visibility.

This is where NetSuite + FullClarity delivers a powerful, future-proof solution. Built natively on the #1 Cloud ERP, our platform automates complex job costing and WIP reporting, transforming your data into a real-time 'single source of truth'. You gain the power to eliminate margin erosion before it happens and confidently steer your projects toward greater profitability.

Stop reacting to financial surprises and start proactively driving your business forward. Gain FullClarity on Your Project Financials. Request a Demo.

Frequently Asked Questions About Construction Revenue Recognition

What is the difference between revenue recognition and billing in construction?

Billing is the process of invoicing a client based on the contract's payment schedule, directly impacting your company's cash flow. In contrast, revenue recognition is an accounting principle that dictates when you can record that income on your financial statements. Revenue is recognized as performance obligations are satisfied (i.e., as work is completed), which often does not align perfectly with billing cycles. This distinction is crucial for accurate financial reporting and performance analysis.

How does ASC 606 specifically affect construction change orders?

Under ASC 606, a change order must be evaluated to determine if it creates a new performance obligation or modifies the existing one. If the scope change is distinct and priced at its standalone selling price, it's treated as a new contract. Otherwise, it modifies the original contract's transaction price and measure of progress. This requires a robust system to track changes and ensure revenue is recognized accurately, preventing margin erosion on complex projects.

Under what circumstances can a construction company use the Completed Contract method?

The Completed Contract method is rarely permissible under current accounting standards like ASC 606. Its use is restricted to contracts that are short-term in nature, typically completed within a single fiscal year. It may also be used in rare situations where the outcome of a project cannot be reasonably estimated. For most long-term projects, the Percentage of Completion method is required to provide a more accurate and timely view of a company's financial performance.

What is a Work-in-Progress (WIP) schedule and how does it relate to revenue recognition?

A Work-in-Progress (WIP) schedule is a critical financial report that provides a real-time overview of your projects' health. It compares the percentage of work completed and costs incurred against what has been billed to the client. This report is the engine for accurate construction revenue recognition, as it calculates overbillings and underbillings, allowing you to recognize revenue precisely in line with project progress and ensure your financial statements are a single source of truth.

How does financial retainage impact revenue recognition under ASC 606?

ASC 606 treats retainage as a form of "variable consideration." This means you must estimate the amount of retainage you expect to ultimately collect and include it in the total transaction price from the project's outset. Revenue from this estimated retainage is then recognized proportionally as you complete the work-not when the cash is finally paid upon completion. This provides a more accurate, real-time picture of project profitability and financial standing.

Can our firm switch between revenue recognition methods for different projects?

No, consistency is a fundamental accounting principle. Your firm must establish a single, appropriate revenue recognition policy for similar types of contracts and apply it consistently across all of them. Switching between methods like Percentage of Completion and Completed Contract for different projects is not compliant with GAAP. This consistency ensures that your financial statements are reliable, comparable, and provide clear visibility into your company’s true performance over time.

- Hero Image")